In 10 days, I will present a recent research in the French/Japanese conference on Asian and International Economies in an Era of Globalization. In this research, we use time-varying causality tests. So today, I will show how to use the time-varying Granger causality tests introduced by Barbara Rossi and Yiru Wang in 2019:

Rossi, B., & Wang, Y. (2019). Vector autoregressive-based Granger causality test in the presence of instabilities. The Stata Journal, 19(4), 883-899.

We are going to replicate the results of Appendix in the following article:

Afonso, A., Mignon, V., & Saadaoui, J. (2024). On the time-varying impact of China’s bilateral political relations on its trading partners:“Doux commerce” or “trade follows the flag”? China Economic Review, 85, 102184.

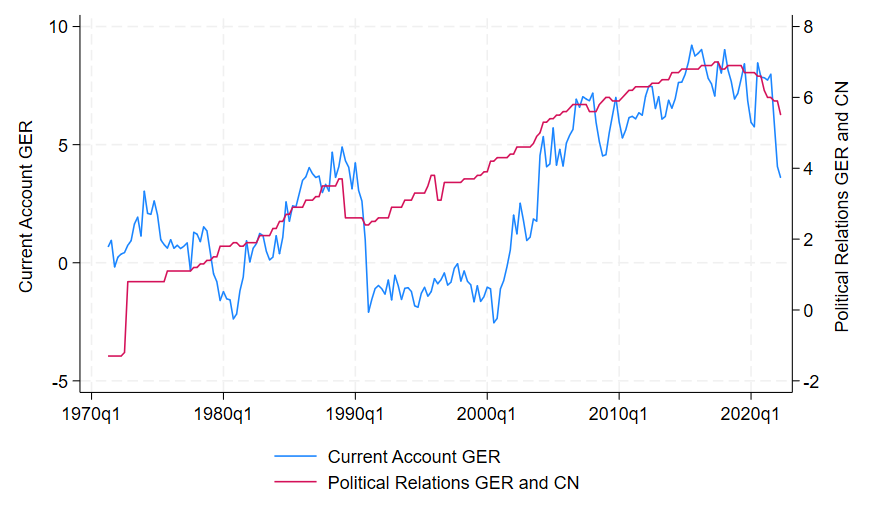

First things first, let us take a look at the two series:

The alternative approach proposed by Rossi and Wang (2019) to test Granger non-causality in the presence of instability in the case of the following two relationships (lpriger, is the index of political relationships between China and Germany; curger, is the current account balance of Germany; xrger, is the exchange rate, EUR/USD):

lpriger \xrightarrow{\mathrm{GC} ?} xrger

\\

lpriger \xrightarrow{\mathrm{GC} ?} cabger.Small remark: As recommended by Andrew Sun, use the [ latex ]...[ /latex ] shortcode to insert an inline equation on WordPress if you are using the KaTeX plugin:

andrewsun.com/projects/wp-katex/

Firstly, their approach consists in using a reduced-form VAR with time-varying parameters,

\begin{aligned}

A_t(L) \mathbf{y}_t & =\mathbf{u}_t \quad \text{(A.1)}\\

A_t(L) & =\mathbf{I}-\mathbf{A}_{1, t} L-\cdots-\mathbf{A}_{p, t} L^p \\

\mathbf{u}_t & \stackrel{\text { i.i.d}}{\sim}(\mathbf{O}, \mathbf{\Sigma})

\end{aligned}where \mathbf{y}_{t}=\left[y_{1, t}, y_{2, t}, \ldots, y_{n, t}\right]^{\prime} is an (n \times 1) vector and \mathbf{A}_{j, t}, j=1, \ldots, p, are (n \times n) time-varying coefficient matrices.

Secondly, they also consider a direct multistep VAR-LP (LP stands for Local Projection) forecasting with time-varying parameters. By iterating (A.1), \mathbf{y}_{t+h} can be projected onto the linear space generated by \left(\mathbf{y}_{t-1}, \mathbf{y}_{t-2}, \ldots, \mathbf{y}_{t-p}\right)^{\prime}, specifically,

\mathbf{y}_{t+h}=\boldsymbol{\Phi}_{1, t} \mathbf{y}_{t-1}+\cdots+\boldsymbol{\Phi}_{p, t} \mathbf{y}_{t-p}+\boldsymbol{\epsilon}_{t+h} \quad \text{(A.2)}where \boldsymbol{\Phi}_{j, t}, j=1, \ldots,p are functions of \mathbf{A}_{j, t}, \quad j=1, \ldots, p in (A.1) and \boldsymbol{\epsilon}_{t+h} is a moving average of the errors \mathbf{u} from time t to t+h in (A.1) and therefore uncorrelated with the regressors but serially correlated itself.

Let \boldsymbol{\theta}_t be an appropriate subset of \operatorname{vec}\left(\boldsymbol{\Phi}_{1, t}, \boldsymbol{\Phi}_{2, t}, \ldots, \boldsymbol{\Phi}_{p, t}\right). The null hypothesis of the Granger causality robust test is

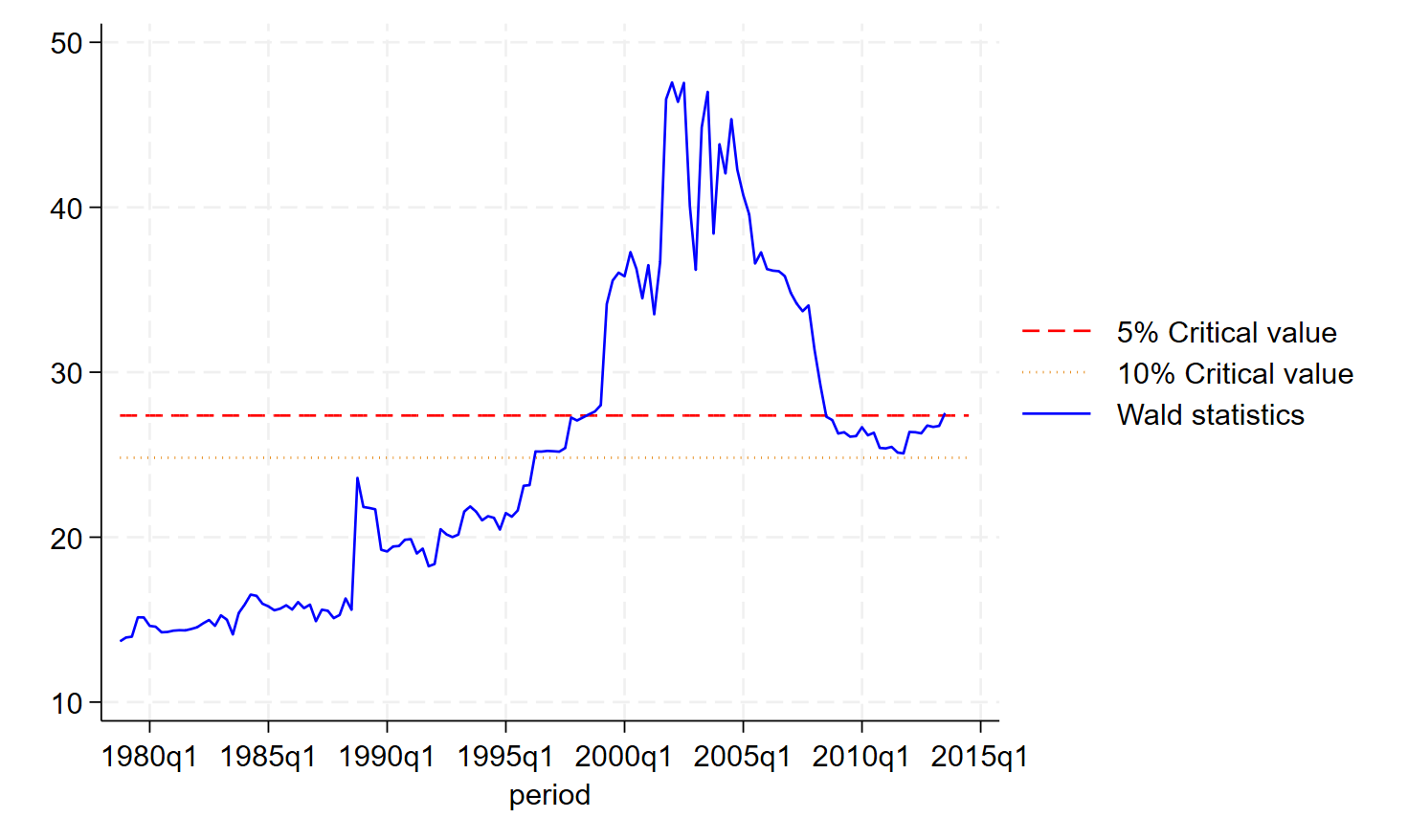

H_0: \boldsymbol{\theta}_t=\mathbf{0}\quad\forall t=1,2 \ldots T \quad \text{(A.3)}The statistics to test H0 in (A.3), presented in Rossi (2005), are ExpW* (the exponential Wald test), MeanW* (the mean Wald test), Nyblom* (the Nyblom test), and QLR* (the Quandt likelihood-ratio test).

The archive describes very well the file available for the replication, so I reproduce the read.me file below:

----------------------------------------------------------------------------

Guidance for implementation:

pvtable.mmat is the file storing pvalue tables;

gcrobustvar.ado is the command to run the VAR-based Granger-causality robust test. There are three commands used in gcrobustvar.ado: chowgmmstar3.ado, nyblomstar3.ado, pvcalc.ado.Let us take a look at the full code, where each important step is commented:

*******************************************************

* Store the data in the same folder as the code and programs

use quaterly_dataset_all_wald_17aug2023.dta, clear

*Drop missing variables

drop if period<tq(1971q1)

drop if period>tq(2022q2)

** Drop the starting value to not have missing values

drop if period<tq(1971q2)

gen trend=_n

****************************************************************

twoway line cur_ger period if period>=00, yaxis(1) || ///

line pri_ger_cn period if period>=00, yaxis(2) ///

legend(pos(6)) xtitle("") ///

name(cur_pri_china_ger, replace)

* Install package

/*

net from http://www.stata-journal.com/software/sj19-4/

net describe st0581

net install st0581, force

net get st0581, force

*/

* Load the critical values

mata:

mata clear

mata matuse pvtable, replace

st_matrix("r(pvap0opt)",pvap0opt)

st_matrix("r(pvapiopt)",pvapiopt)

st_matrix("r(pvnybopt)",pvnybopt)

st_matrix("r(pvqlropt)",pvqlropt)

end

matrix pvap0opt=r(pvap0opt)

matrix pvapiopt=r(pvapiopt)

matrix pvnybopt=r(pvnybopt)

matrix pvqlropt=r(pvqlropt)

* Don't forget to install matsqrt

/*

quietly ///

net describe matsqrt, from(http://www.stata.com/users/jpitblado)

quietly net install matsqrt

*/

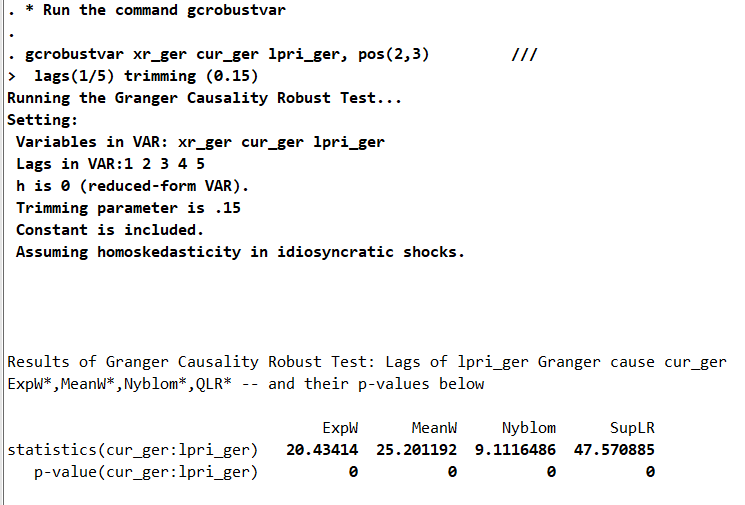

* Run the command gcrobustvar

gcrobustvar xr_ger cur_ger lpri_ger, pos(2,3) ///

lags(1/5) trimming (0.15)

graph rename Graph lpri_ger_cur_ger, replace

* Export the figure

graph export lpri_ger_cur_ger_blog.png, replace ///

name(lpri_ger_cur_ger)

graph export lpri_ger_cur_ger_blog.pdf, replace ///

name(lpri_ger_cur_ger)

*******************************************************

If you want to run the command a second time, you may have to create a Do-file, that I called gc_robust.do:

*Store the data in the same folder as the code and programs

use quaterly_dataset_all_wald_17aug2023.dta, clear

*Drop missing variables

drop if period<tq(1971q1)

drop if period>tq(2022q2)

** Drop the starting value to not have missing values

drop if period<tq(1971q2)

gen trend=_n

mata:

mata clear

mata matuse pvtable, replace

st_matrix("r(pvap0opt)",pvap0opt)

st_matrix("r(pvapiopt)",pvapiopt)

st_matrix("r(pvnybopt)",pvnybopt)

st_matrix("r(pvqlropt)",pvqlropt)

end

matrix pvap0opt=r(pvap0opt)

matrix pvapiopt=r(pvapiopt)

matrix pvnybopt=r(pvnybopt)

matrix pvqlropt=r(pvqlropt)Then, I run a second time the command for the VAR-LP:

* VAR-LP

quietly do gcrobust_blog.do

/*

Run this to not have the error message:

variable time_chowgmmstar not found

*/

gcrobustvar xr_ger cur_ger lpri_ger, pos(2,3) ///

lags(1/5) trimming (0.15) horizon(5)

graph rename Graph lpri_ger_cur_ger, replaceAfter the mid-1990s, we reject the null of non-causality. The trade always follows the flag between Germany and China. Montesquieu may be wrong:

4 Comments

I am still getting the error: variable time_chowgmmstar not found

See the last part of the blog:

“If you want to run the command a second time, you may have to create a Do-file, that I called gc_robust.do:”

Thank you very much Proff, it worked. I have been struggling for days.

You’re welcome Jason.

Please don’t hesitate to ask something else.