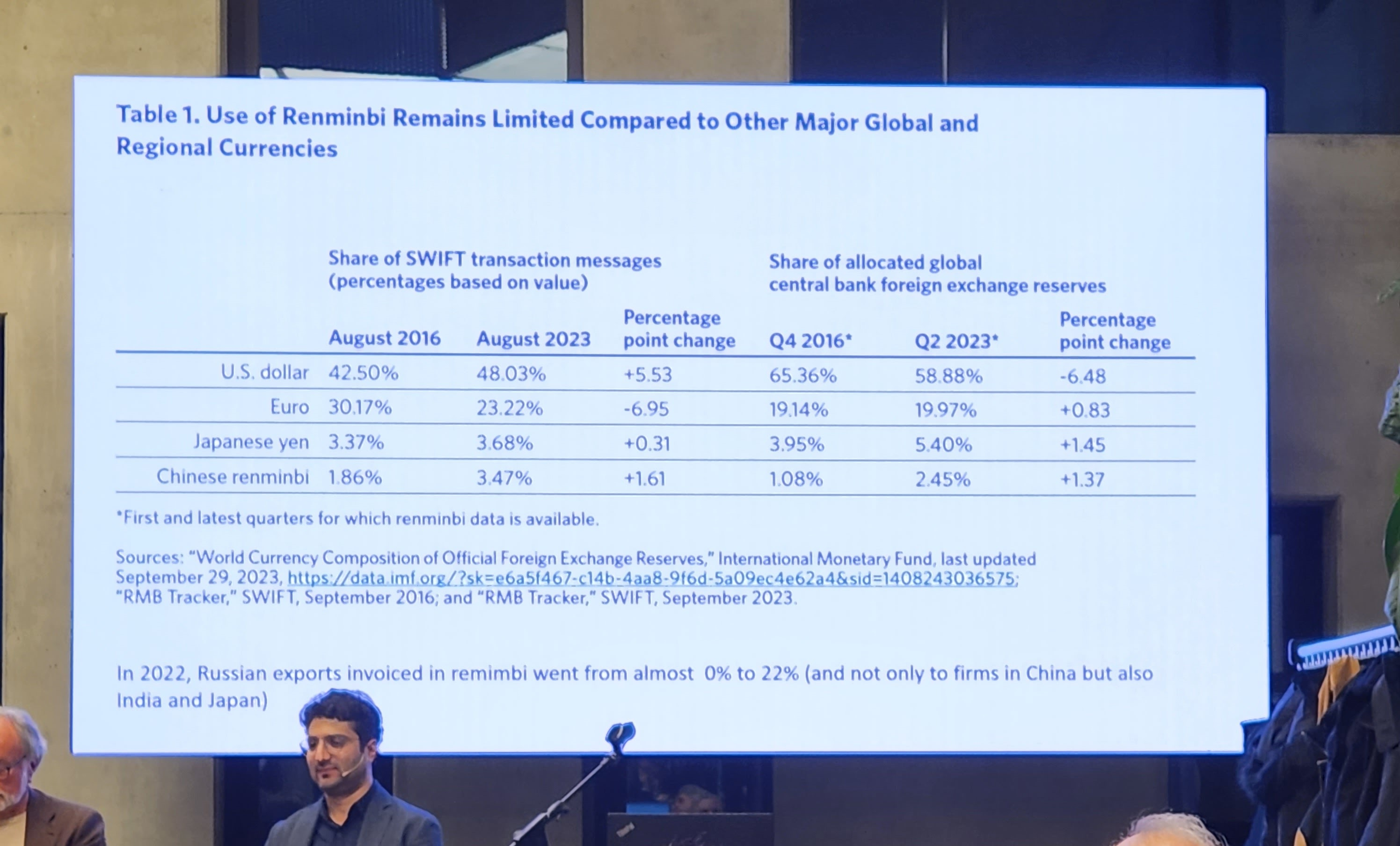

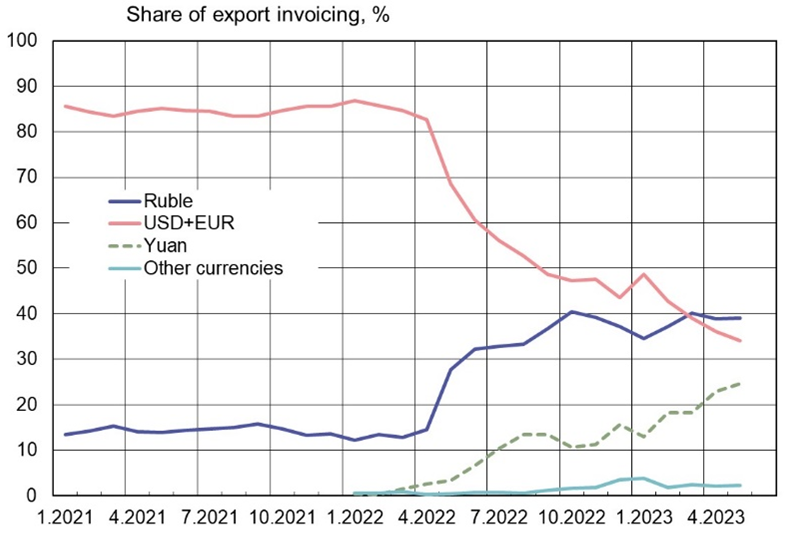

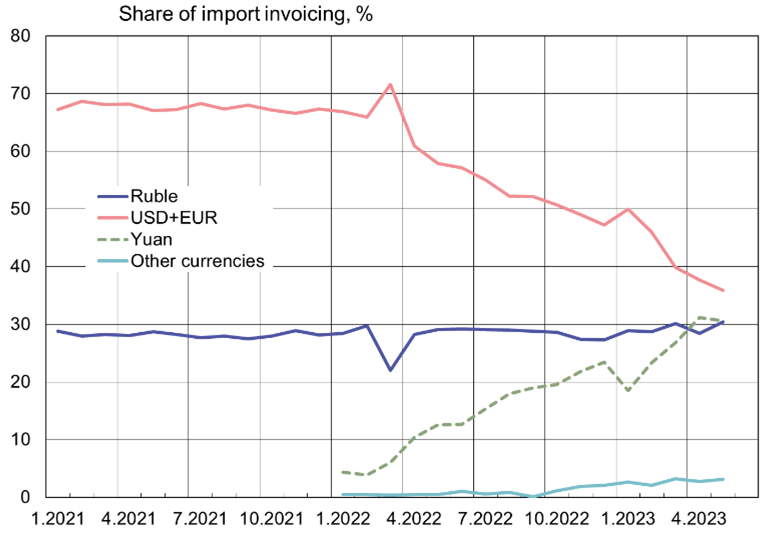

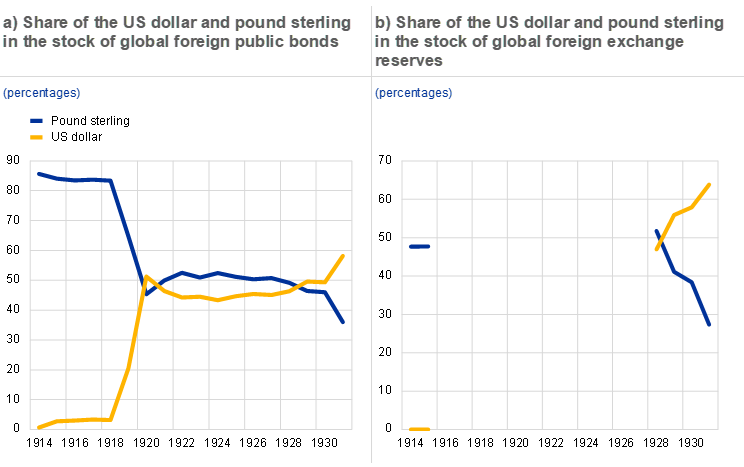

During the 16th FIW conference, I had the chance to attend the policy panel on the “Tectonic shifts in the international economic order”. Giorgia Giovannetti gave us some insight on the use of renminbi in international trade (see Figure 1). The use of renminbi remains limited in international trade, except in Russia, where 20% of imports are invoiced in renminbi in 2022. This trend is expected to continue (see the Figures 3 and 4). Despite these recent evolutions, the international role of the US dollar is expected to stay the more or less the same in future years, as shown in a recent paper by Menzie Chinn, Jeffrey A. Frankel, and Hiro Ito. So much ado about nothing… for the near future. After all, the Pound Sterling remained dominant for a long time after the demise of the UK as the dominant world power (see Figure 4), at the same time, the competition is stronger in the current period than after WWII, especially with the BRICS group.

Source: https://www.bofit.fi/

Source: https://www.bofit.fi/

Source: https://www.ecb.europa.eu/

1 Comment

[…] overthrown the UK in terms of GDP far before the US dollar became the dominant currency, see this post. Consequently, the dynamics can be highly nonlinear and periods of apparent tranquility can be […]