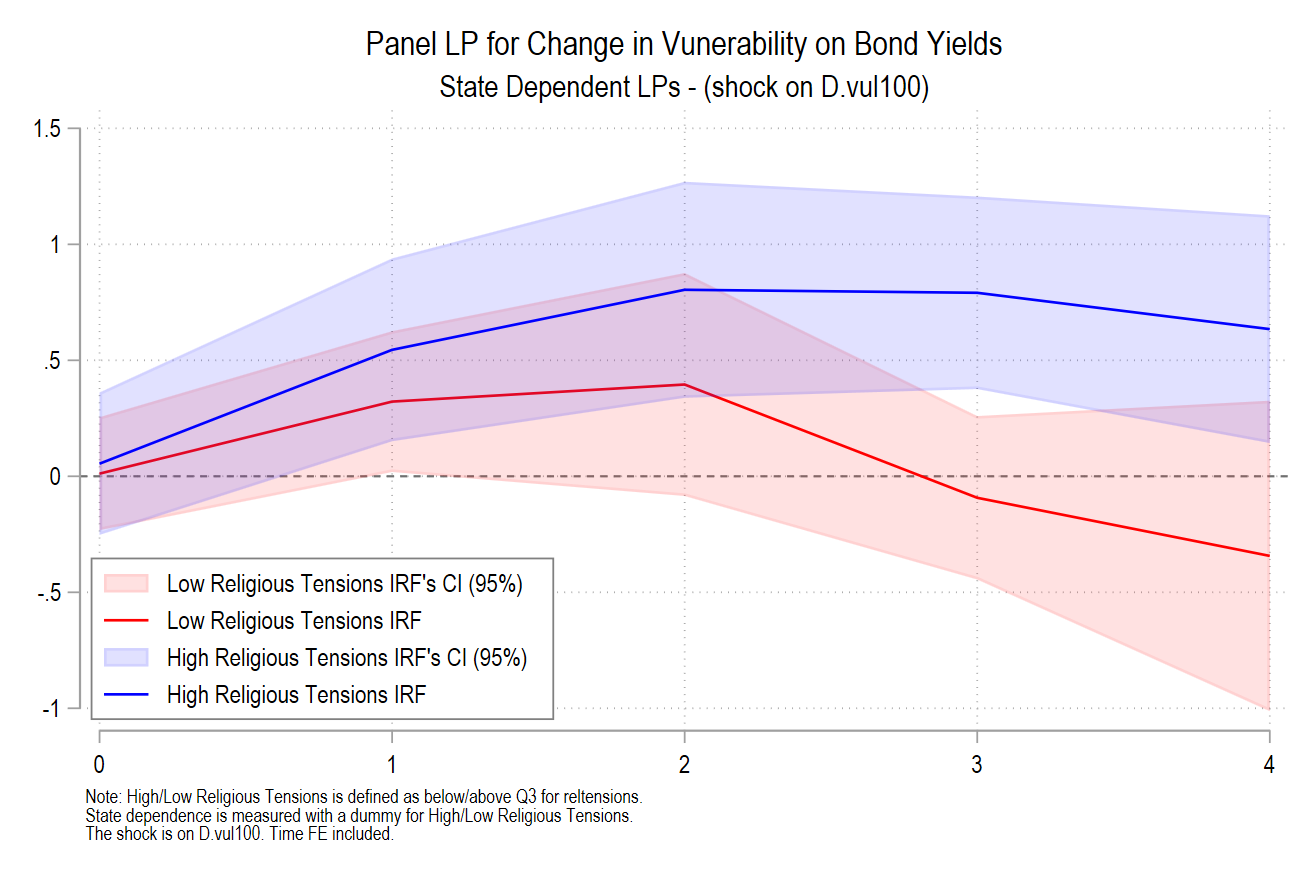

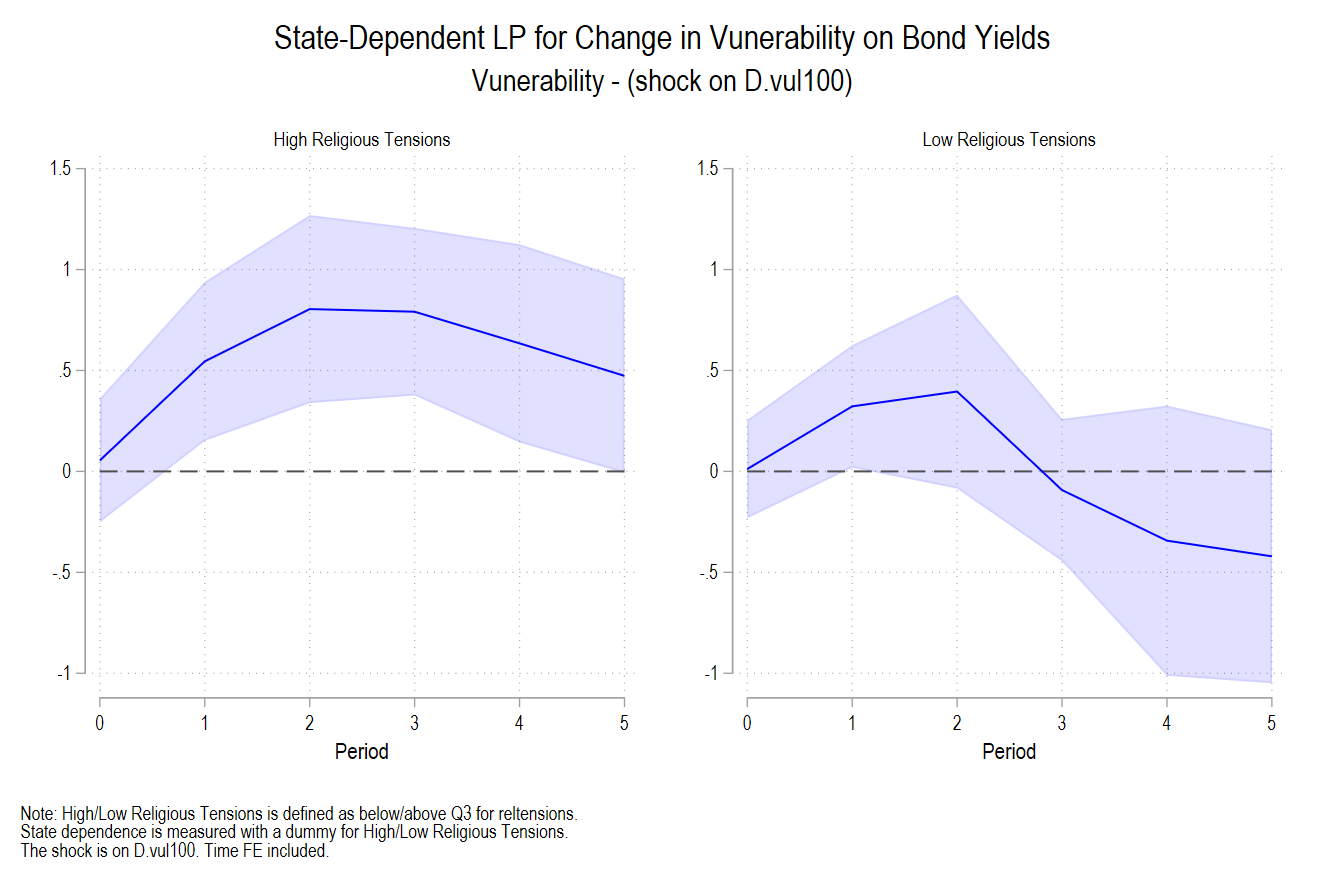

In a previous blog, I covered the estimation of state-dependent local projection using LOCPROJ. The impact of random shocks of change in vulnerability affects positively the sovereign bond yields. The empirical results for different regimes of religious tensions are very similar when I rely on subsamples or on state-dependent local projections:

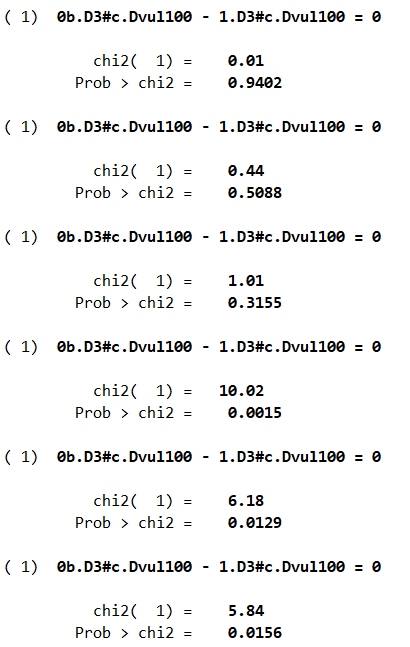

Rodolphe Desbordes on LinkedIn recommended me to test the statistical difference between the two regimes. Relying on the LOCPROJ package, I noticed that the routine keeps in memory the estimates for the last horizon. Thus, using this useful feature, I can program a loop to run a Wald test of equality for the coefficients in the two regimes at each horizon:

**# Test Religious Tensions

forvalues v = 0(1)5{

qui locproj bonds_tw D3#c.Dvul100, lcs(1.D3#c.Dvul100) ///

h(`v') yl(1) sl(1) ///

c(l(1).CAB l(1).cpi_tw ///

l(1).GDebt l(1).GDeficit ///

l(1).banking l(1).currency ///

l(1).debt i.period) ///

fe cluster(imfcode) conf(95) ///

title(`"High Vulnerability"') ///

save irfname(belowbv) zero ///

stats nograph

test (_b[0.D3#c.Dvul100] = ///

_b[1.D3#c.Dvul100])

}

From horizon 3 to 5, the impulse response functions are statistically significant different from each other. The climate risk premium is higher in countries and during periods of high religious tensions.

The latest version of the slides is available in this post.