After some insightful email exchanges with Lutz Kilian, I was wondering whether oil market uncertainty and geopolitical risk are related. To measure oil market uncertainty, I use the Cboe Crude Oil ETF Volatility Index (OVX) coming from the Cboe website. The definition is given on their website:

“The Cboe Crude Oil ETF Volatility IndexSM (OVX) is an estimate of the expected 30-day volatility of crude oil as priced by the United States Oil Fund (USO). Like the Cboe VIX Index®, OVX is calculated by interpolating between two time-weighted sums of option mid-quote values – in this case, options on the USO ETF. The two sums essentially represent the expected variance of the price of crude oil up to two option expiration dates that bracket a 30-day period of time. OVX is obtained by annualizing the interpolated value, taking its square root and expressing the result in percentage points.”

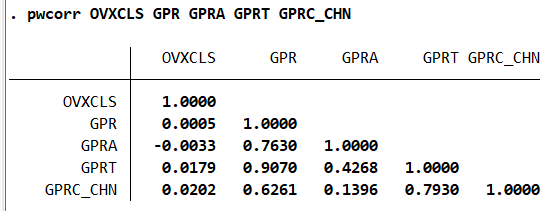

I aggregate the indexes to have monthly data using the mean and compute the correlation between the oil market uncertainty (OVX) and geopolitical risks (GPR).

So what about the correlation between oil market uncertainty and the GPR index that comes from Matteo Iacoviello’s website? For the whole sample, the correlation is very low.

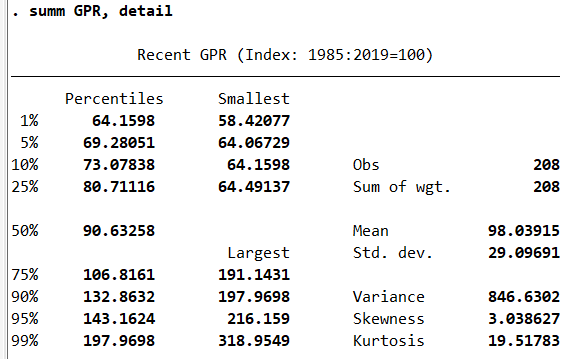

However, it may be very probable that the correlation is nonlinear and kicks in only when the GPRs are elevated. Let us take a look at the distribution of the GPRs:

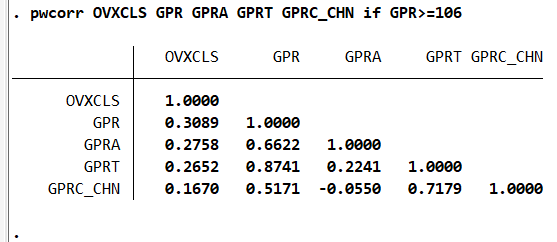

What about the correlation to the values above the third quartile for the overall GPR? The correlation increases to around 30 percent between the OVX and the overall GPR.

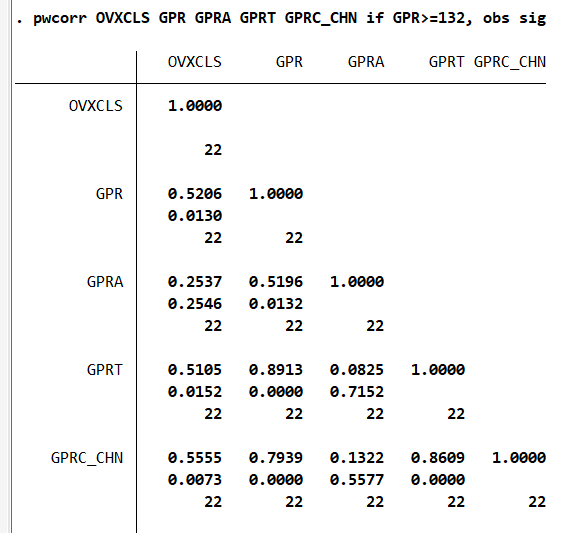

What about the correlation to the values above the ninth decile for the overall GPR? The correlation between the OVX index and the overall GPR jumps from 30 percent to 50 percent. Besides, the correlation to the GPR specific to China has the highest value, above 55 percent. The correlation for GPR acts is twice lower.

Overall, GPR may drive oil market uncertainty only during amidst elevated levels of geopolitical risks.

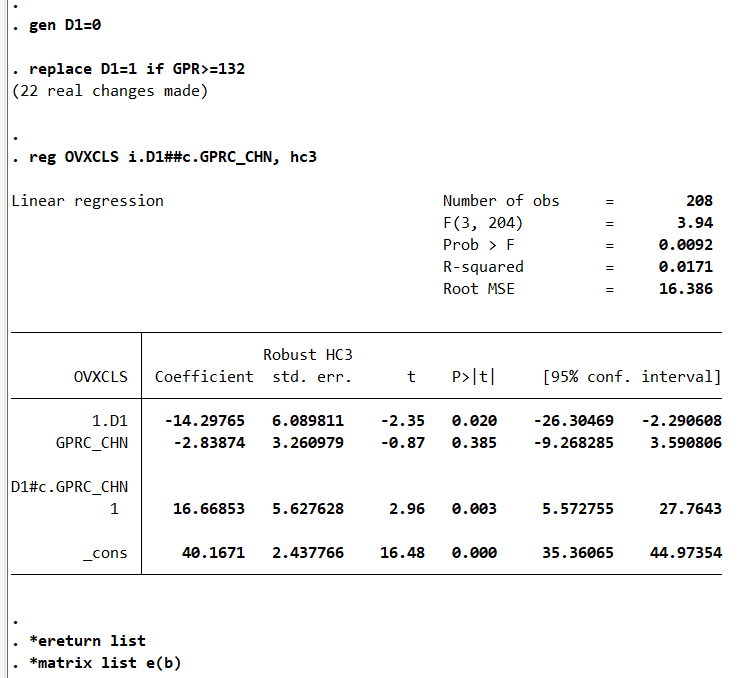

As an illustration, we can create a dummy for the high geopolitical risk regime and run a regression on the OVX index. An increase of 1 percent in the GPR specific to China induces an increase in 13 percent of the OVX index (less than one standard deviation for OVX and the regression does not include any controls):

gen D1=0

replace D1=1 if GPR>=132

reg OVXCLS i.D1##c.GPRC_CHN, hc3

*ereturn list

*matrix list e(b)

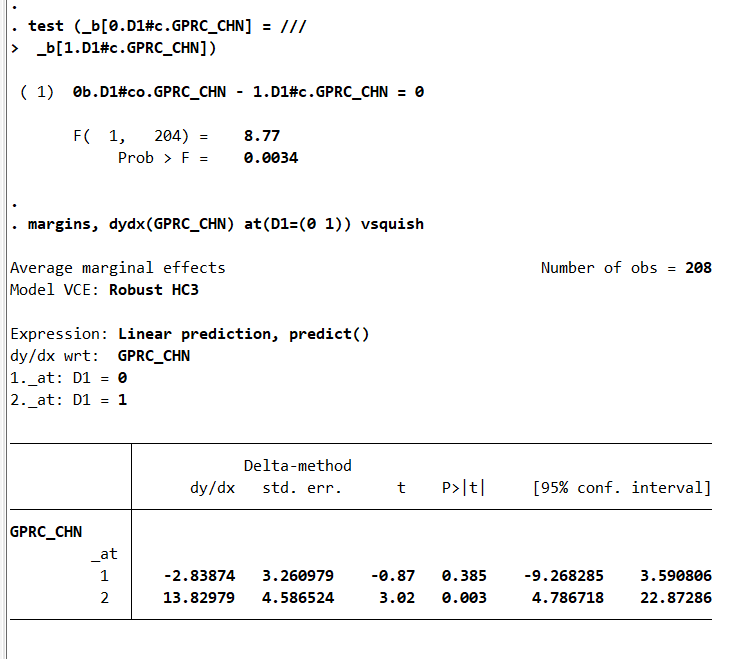

test (_b[0.D1#c.GPRC_CHN] = ///

_b[1.D1#c.GPRC_CHN])

margins, dydx(GPRC_CHN) at(D1=(0 1)) vsquish