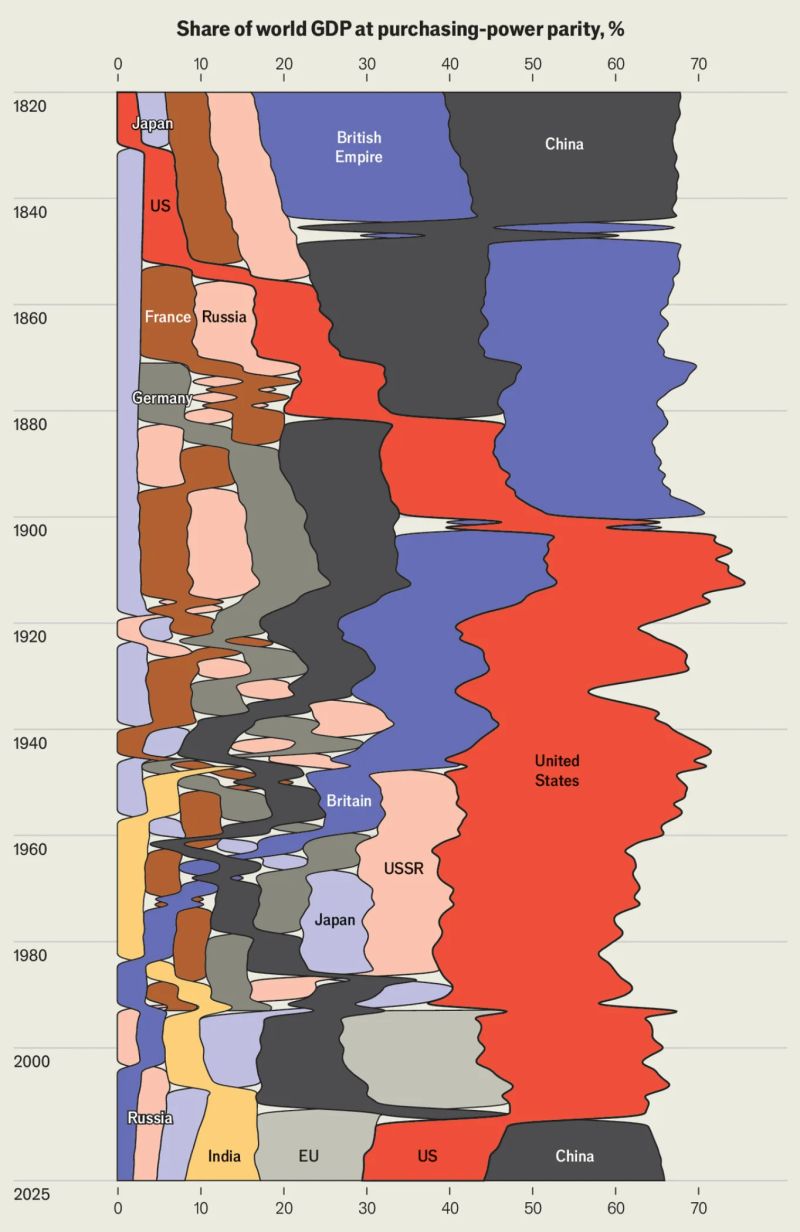

The chart from The Economist offers a useful starting point for thinking about the long-run redistribution of global economic power. It shows the share of world GDP at purchasing-power parity, from the early nineteenth century to the present, and the visual message is clear: the United States remains powerful, but its relative economic dominance is no longer what it was. The Economist published the figure in its interactive feature “America is mighty—but becoming less dominant”, and the chart uses long-run and contemporary data sources including the Maddison Project Database, World Bank, IMF, Colonial Dates Dataset, and The Economist’s own calculations.

Source: The Economist, “America is mighty—but becoming less dominant”. Underlying sources listed by the chart include the Maddison Project Database 2023, Colonial Dates Dataset 2019, World Bank, IMF, and The Economist. Note: the figure compares countries, empires, and blocs, so it should be read as a geopolitical-economic visualization rather than as a strictly country-by-country GDP ranking.

Purchasing-power parity matters because it asks a different question from market exchange-rate GDP. It does not simply measure how much an economy is worth at current exchange rates; it tries to compare the real volume of goods and services that economies can produce after adjusting for price-level differences. The World Bank explains that PPP-based comparisons are more appropriate than exchange-rate comparisons when the goal is to compare the real size of economies and average material well-being.

The chart can be read through the lens of Branko Milanović’s recent book, The Great Global Transformation. In the UK edition, the subtitle is National Market Liberalism in a Multipolar World; in the U.S. edition, it is The United States, China, and the Remaking of the World Economic Order. Milanović’s central claim is that globalization has produced a major reshuffling of global incomes, driven especially by the rise of Asia and China, and that this has weakened the old neoliberal order. The University of Chicago Press describes the book as an account of a new era of national market liberalism, in which markets remain important domestically, but international economic relations become more nationalist, protectionist, and geopolitical.

This framework helps us compare three different rivalries: the U.S.–USSR rivalry before the 1980s, the U.S.–Japan rivalry of the 1970s and 1980s, and the current U.S.–China rivalry. These rivalries are often discussed together, but they were macroeconomically very different.

1. The U.S.–USSR rivalry: military symmetry, economic asymmetry

Before the 1980s, the main geopolitical rivalry was between the United States and the Soviet Union. This was a rivalry between two political-economic systems: market capitalism and central planning. The Soviet Union could mobilize enormous resources for heavy industry, defence, space technology, and geopolitical influence. It was a military superpower and an ideological competitor.

But it was not a full economic peer of the United States. U.S. government assessments already pointed to the structural weaknesses of the Soviet economy. A CIA paper from December 1982, reproduced by the U.S. State Department’s Office of the Historian, expected Soviet GNP growth to fall below 2 percent per year in the 1980s, citing slower labour-force growth, declining productivity gains, energy constraints, agricultural instability, and the burden of defence spending.

The economic comparison was also methodologically difficult. A later GAO assessment noted that CIA estimates of Soviet GNP relied on purchasing-power comparisons but were likely affected by serious limitations, especially the inferior quality and limited variety of Soviet goods and services. In other words, even when Soviet output looked large in aggregate, it did not translate into the same level of consumer welfare, technological dynamism, or productive efficiency as in the United States.

The macroeconomic logic of the Cold War was therefore unusual. The USSR was a geopolitical and military peer, but not an economic peer in the broader sense. It could challenge U.S. strategic power, but it could not organize the global economy around the Soviet model. The rivalry took place between two blocs with relatively low economic interdependence. Trade, capital flows, technology transfer, and financial integration between the two systems were limited.

This was a rivalry of systems, armies, and resource mobilization. The central macroeconomic question was whether central planning could sustain enough growth, innovation, and military capacity to compete with advanced capitalism. It could do so for a time in selected sectors, but not across the whole economy. The Soviet model was strong in mobilization but weak in productivity, incentives, consumer welfare, and technological diffusion.

2. The U.S.–Japan rivalry: industrial fear inside the capitalist camp

The U.S.–Japan rivalry was very different. Japan was not an ideological enemy of the United States. It was a U.S. security ally, a capitalist economy, and part of the U.S.-led international order. Yet by the late 1970s and 1980s, Japan’s rise generated deep anxiety in Washington.

Japan’s challenge was industrial rather than military. It came through cars, electronics, machine tools, semiconductors, export discipline, high savings, and highly competitive firms. The fear was not that Japan would replace capitalism with another system. The fear was that Japan might outperform American capitalism inside the capitalist system itself.

The macroeconomic tension appeared in exchange rates and trade balances. The 1985 Plaza Accord was a coordinated G5 initiative to reverse an overvalued dollar. Jeffrey Frankel’s NBER study describes it as a successful effort to bring down the dollar and reduce the U.S. trade deficit. The IMF notes that after the accord, the yen appreciated sharply, and Japan’s export and GDP growth essentially halted in the first half of 1986.

Semiconductors were already central to this rivalry. Douglas Irwin’s study of the U.S.–Japan semiconductor dispute describes the 1986 semiconductor agreement as one of the most controversial U.S. trade-policy actions of the 1980s. Japan agreed to address semiconductor dumping and to help secure a 20 percent foreign share of its domestic semiconductor market.

But the Japan rivalry remained manageable because it occurred within a shared geopolitical framework. Japan did not lead a rival military bloc. It did not offer a competing universal ideology. It did not seek to dismantle the U.S.-led international order. The conflict could therefore be handled through exchange-rate coordination, trade negotiations, foreign direct investment, and institutional bargaining.

This was a rivalry of factories, exchange rates, and industrial policy. The central macroeconomic question was whether U.S. manufacturing could remain competitive against a highly efficient export-oriented capitalist economy. It was serious, but it did not threaten to split the world economy into rival geopolitical blocs.

3. The U.S.–China rivalry: the Soviet and Japanese challenges combined

The current U.S.–China rivalry is more complex because it combines elements of both earlier rivalries.

China resembles Japan in one respect: it has become a major industrial and technological competitor through export capacity, manufacturing scale, infrastructure investment, and technological upgrading. China’s rise has changed global production networks in a way that Japan’s rise also did, but on a much larger scale.

China also resembles the Soviet Union in another respect: it is a strategic and systemic competitor of the United States. It has a different political regime, a powerful state, a large military, and a geopolitical project that does not simply accept U.S. primacy.

But China is also different from both Japan and the Soviet Union. Unlike Japan, China is not a U.S. security ally. Unlike the Soviet Union, China is deeply integrated into global capitalism. It is central to trade, manufacturing, supply chains, infrastructure, and increasingly technology. The WTO reports that in 2024 China was the world’s largest merchandise exporter, with exports of $3.58 trillion, while the United States remained the world’s largest importer, with imports of $3.36 trillion.

This creates a new kind of rivalry: geoeconomic competition under deep interdependence. The United States and China compete strategically, but they are also connected through trade, finance, supply chains, universities, firms, standards, and technology ecosystems. This makes decoupling costly and difficult, but it also makes interdependence politically sensitive.

The U.S. response has shifted from classical globalization to economic security. USTR’s Section 301 investigation focused on China’s practices related to technology transfer, intellectual property, and innovation. The Bureau of Industry and Security later imposed export controls on advanced computing chips, semiconductor manufacturing equipment, and supercomputer-related transactions involving China, explicitly linking these controls to U.S. national-security and foreign-policy concerns.

This is exactly the type of world Milanović describes. Global neoliberalism does not disappear completely; markets, firms, profits, and competition remain central. But the international order becomes more national, more fragmented, and more security-driven. The result is not classical free trade, but national market liberalism: domestic markets plus strategic external controls.

Three rivalries compared

| Rivalry | Main period | Nature of the challenge | Degree of economic interdependence | Main macroeconomic issue |

|---|---|---|---|---|

| U.S.–USSR | 1945–1980s | Ideological, military, systemic | Low | Could central planning mobilize enough resources to compete with capitalism? |

| U.S.–Japan | 1970s–1990s | Industrial, commercial, technological | High, but inside the U.S. alliance system | Could U.S. manufacturing compete with Japanese export capitalism? |

| U.S.–China | 2000s–today | Industrial, technological, geopolitical, systemic | High, but politically contested | Can the U.S. preserve leadership when China is both a production hub and a strategic rival? |

The table shows why the present moment is so difficult. The Soviet Union was militarily dangerous but economically less integrated. Japan was economically threatening but geopolitically aligned. China is both economically central and geopolitically autonomous.

The macroeconomic lesson: relative decline is not absolute decline

The Economist chart should not be read as a simple story of American collapse. A country can continue to grow, innovate, and remain rich while its share of world GDP declines. This happens when other economies grow faster. Relative decline is therefore partly a mathematical consequence of convergence.

This distinction is crucial. The United States remains powerful in technology, finance, military capacity, higher education, energy, capital markets, and global institutions. But its share of world output at PPP has fallen because China, India, and other emerging economies have grown rapidly. In macroeconomic terms, the denominator has changed.

Milanović’s contribution is to connect this macroeconomic convergence to political transformation. The rise of Asia has not only shifted GDP shares. It has also changed the global income distribution. Large numbers of people in Asia have moved upward in the world income hierarchy, while parts of the Western middle class have experienced relative stagnation or status anxiety. This helps explain why globalization produced both global convergence and domestic political backlash.

Why China is not simply “the new Japan”

The comparison with Japan is useful but incomplete. Like Japan in the 1980s, China has generated anxiety through manufacturing competitiveness, trade surpluses, and technological upgrading. But China’s scale is much larger, and its political position is fundamentally different.

Japan’s challenge was largely absorbed into the U.S.-led order. Japanese firms invested in the United States. Exchange-rate coordination reduced some tensions. Trade disputes were intense but negotiable. Japan remained a U.S. ally.

China is not likely to be absorbed in the same way. It is too large, too politically distinct, and too central to the world economy. Its rise changes not only trade flows but also the distribution of global power. This is why the U.S.–China rivalry cannot be managed only through exchange-rate agreements or sectoral trade deals.

Why China is not simply “the new Soviet Union”

The Soviet comparison is also useful but incomplete. Like the USSR, China presents a systemic and geopolitical challenge. But unlike the USSR, China is not outside the world economy. It is one of the main engines of it.

This makes the rivalry more complicated than the Cold War. The United States and the Soviet Union could compete through military blocs with relatively limited mutual economic dependence. The United States and China cannot do this so easily. Their firms, consumers, universities, supply chains, and financial systems have been connected for decades.

The Soviet rivalry was about separation between two systems. The China rivalry is about competition inside a partially shared system.

The return of multipolarity

The chart’s deeper message is that the unipolar moment was historically exceptional. The post-1945 U.S. position reflected extraordinary circumstances: American industrial strength, the destruction of much of Europe and Asia during the Second World War, the dollar-centred monetary order, and the institutional architecture of the postwar period.

That world is changing. The rise of China and Asia does not mean the end of American power. It means the return of a broader distribution of economic weight. The world economy is moving from a period of Western and then American predominance toward a more contested multipolarity.

This transition creates risks. Economic rivalry can lead to tariffs, sanctions, export controls, industrial subsidies, competing standards, and duplicated supply chains. These policies may improve resilience in some sectors, but they can also reduce efficiency, raise costs, and fragment global markets.

Yet the transition also reflects a positive historical development: global convergence. The rise of Asia has lifted hundreds of millions of people into higher levels of income and consumption. The problem is not convergence itself. The problem is whether existing political institutions can manage the distributional and geopolitical consequences of convergence.

Conclusion

The U.S.–USSR rivalry was a contest between military blocs and economic systems. The U.S.–Japan rivalry was a contest over industrial competitiveness inside the same capitalist camp. The U.S.–China rivalry is different because it combines both dimensions: China is an industrial competitor, a technological rival, a geopolitical challenger, and a deeply integrated part of the world economy.

This is why Branko Milanović’s Great Global Transformation is a useful framework for interpreting the chart. The world is not simply moving from American dominance to Chinese dominance. It is moving toward a more complex order in which several large economies compete, cooperate, and try to protect their own national advantages.

The central macroeconomic question is therefore not only who has the largest GDP. It is whether the major powers can manage convergence without destroying the gains from globalization. The Soviet case shows the limits of mobilization without productivity. The Japan case shows that industrial rivalry can be negotiated when the geopolitical framework is shared. The China case is harder because economic and geopolitical rivalry are fused.

The future of the world economy will depend on whether this rivalry produces destructive fragmentation or a new, more balanced form of interdependence. That is the essence of the great global transformation.

References

- Becker, Bastian. 2019. “Introducing COLDAT: The Colonial Dates Dataset.” https://www.beckerbastian.net/data

- Bolt, Jutta, and Jan Luiten van Zanden. 2024. “Maddison Style Estimates of the Evolution of the World Economy: A New 2023 Update.” Maddison Project Database 2023. University of Groningen

- Bureau of Industry and Security. 2022. “Implementation of Additional Export Controls: Certain Advanced Computing and Semiconductor Manufacturing Items; Supercomputer and Semiconductor End Use; Entity List Modification.” Federal Register. Federal Register

- Frankel, Jeffrey A. 2015. “The Plaza Accord, 30 Years Later.” NBER Working Paper No. 21813. NBER

- International Monetary Fund. 2011. “Did the Plaza Accord Cause Japan’s Lost Decades?” World Economic Outlook, Box 1.4. IMF

- Irwin, Douglas A. 1996. “The U.S.–Japan Semiconductor Trade Conflict.” In The Political Economy of Trade Protection. NBER. NBER PDF

- Milanović, Branko. 2025. The Great Global Transformation: National Market Liberalism in a Multipolar World. London: Allen Lane. Penguin

- Milanović, Branko. 2026. The Great Global Transformation: The United States, China, and the Remaking of the World Economic Order. Chicago: University of Chicago Press. University of Chicago Press

- The Economist. 2026. “America is mighty—but becoming less dominant.” Interactive feature, 1 July. The Economist

- United States Department of State, Office of the Historian. 1982. “The State of the Soviet Economy in the 1980s.” CIA paper reproduced in Foreign Relations of the United States, 1981–1988. Office of the Historian

- United States Government Accountability Office. 1991. Soviet Economy: Assessment of How Well the CIA Has Estimated the Size of the Economy. GAO PDF

- United States Trade Representative. 2018. “Section 301 Investigation: China’s Acts, Policies, and Practices Related to Technology Transfer, Intellectual Property, and Innovation.” USTR

- World Bank. “GDP, PPP: Metadata.” World Development Indicators. World Bank DataBank

- World Trade Organization. 2025. Global Trade Outlook and Statistics. WTO PDF