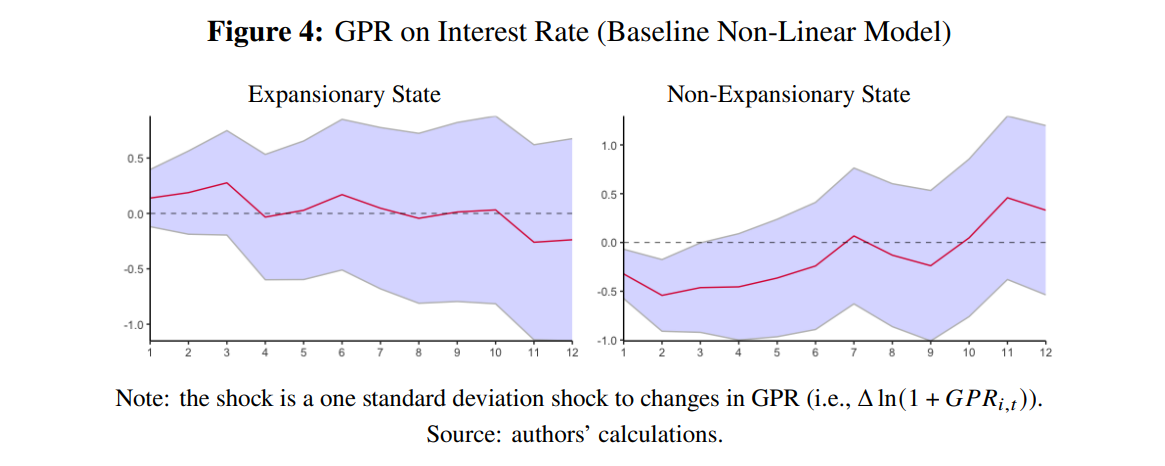

NEW WORKING PAPER: How do geopolitical risk shocks impact monetary policy? Based on a panel of 20 economies, we develop and estimate an augmented panel Taylor rule via linear and nonlinear local projections (LP) regression models. First, the linear model suggests that the interest rate remains relatively unchanged in the event of an uncertainty shock. Second, the result turns out to be different in the nonlinear model, where the policy reaction is muted during an expansionary state, which is operating in a manner proportional to the transitory shock. However, geopolitical risks can amplify the policy reaction during a non-expansionary period.

You are welcome to download, share, or comment on the following working paper:

- William Ginn, Jamel Saadaoui (17 March 2024), Monetary Policy Reaction to Geopolitical Risks: Some Nonlinear Evidence, SSRN Working Paper : https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4762672

1 Comment

[…] How do geopolitical risk shocks impact monetary policy? […]