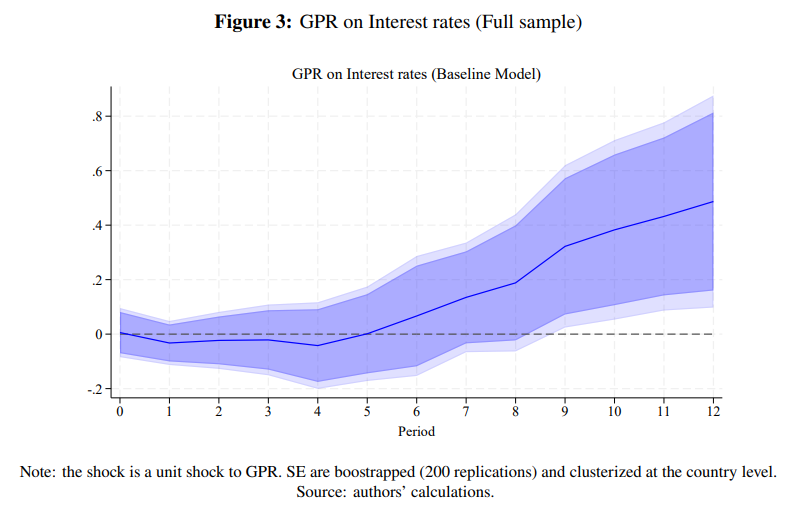

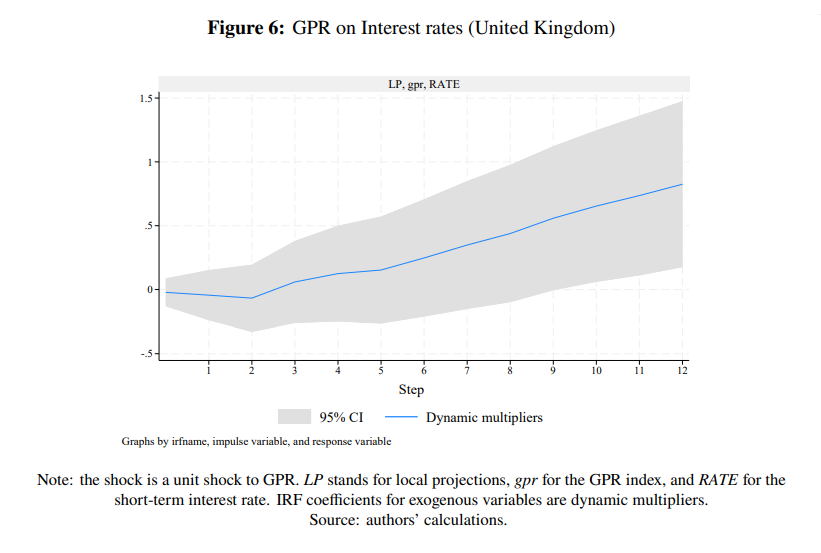

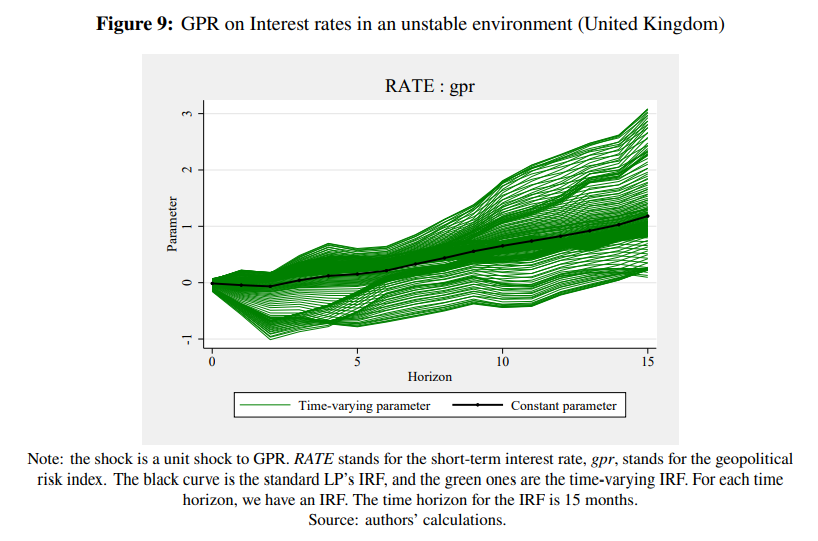

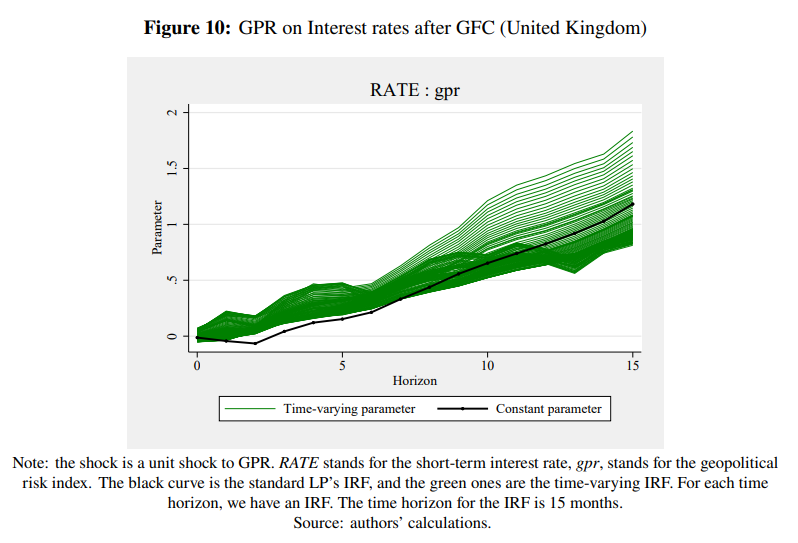

MAJOR WP UPDATE: How do geopolitical risk shocks impact monetary policy? Based on a panel of 20 economies, we develop and estimate an augmented panel Taylor rule via constant and time-varying local projection (TV-LP) regression models. First, the panel evidence suggests that the interest rate decreases in the short run and increases in the medium run in the event of a GPR shock. Second, the results are confirmed in the time-varying model, where the policy reaction is accommodating in the short run (1 to 2 months) to limit risk aversion. In the medium term (12 to 15 months), the central bank is more committed to combating inflation pressures.

You are welcome to download, share, or comment on the following working paper:

- William Ginn, Jamel Saadaoui (27 August 2024), Monetary Policy Reaction to Geopolitical Risks in Unstable Environments, SSRN Working Paper : 4762672.

The previous version was called: “How do geopolitical risk shocks impact monetary policy?” and is described here:

2 Comments

[…] You can find the SSRN version with the abstract and the keywords in an older post. […]

[…] You can find the SSRN version with the abstract and the keywords in an older post. […]