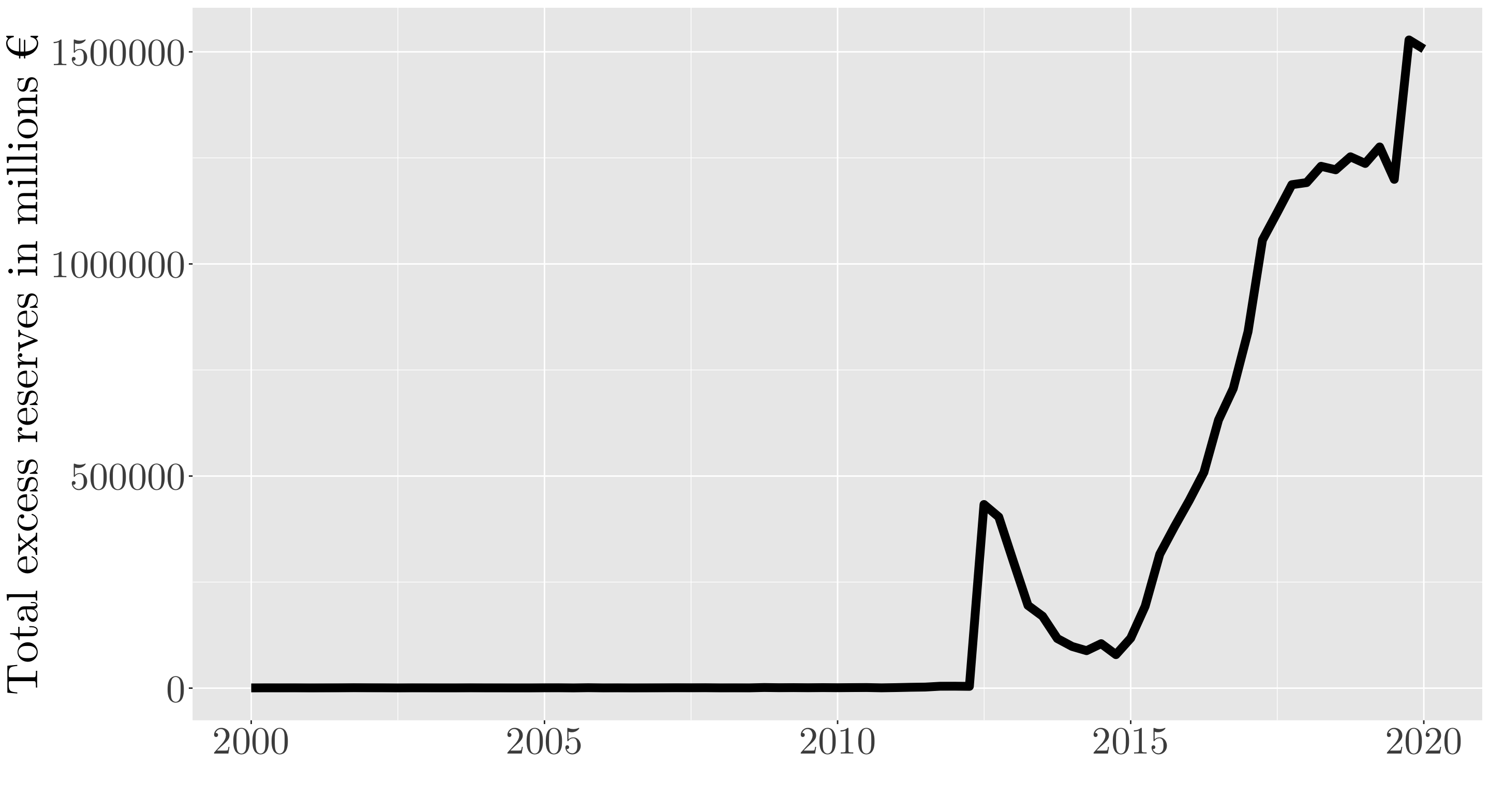

NEW WORKING PAPER: The European Central Bank’s (ECB) quantitative easing (QE) program was supposed to stimulate the real economy and be able to control inflation rates. Nevertheless, primarily the financial sector has benefited from the asset purchase program. Transmission was not taking place as desired, with commercial banks as money creators and thus liquidity distributors at the center of its inefficiency. Accordingly, this article aims to examine the transmission of central bank money to the euro area economy via the banking system and the corresponding bank lending channel (BLC). To bring clarity to the economic debate about the effectiveness of the BLC, bank lending and additional macroeconomic variables are divided into productive and unproductive. We analyze how these areas react to an exogenous monetary policy shock in excess reserves, which is identified using different identification schemes before deploying least-square and penalized local projection (LP) methods. Following the estimation results, it can be concluded that a liquidity increase via quantitative easing cannot stimulate economic activity-enhancing lending in the euro area but, on the contrary, tends to disincentivize it. On the other hand, it drives lending to an unproductive sector. Additionally, this is confirmed by the fact that prices, especially in the housing sector, react significantly positively to a QE shock, whereas, on the contrary, producer prices in the industrial sector and inflation are not affected by unconventional monetary policy.

You are welcome to download, share or comment the following working paper:

- Philipp Roderweis, Jamel Saadaoui, Francisco Serranito (2023), Is Quantitative Easing Productive? The Role of Bank Lending in the Monetary Transmission Process. EconomiX Working Paper 2023-17, https://economix.fr/documents-de-travail/is-quantitative-easing-productive-the-role-of-bank-lending-in-the-monetary-transmission-process/