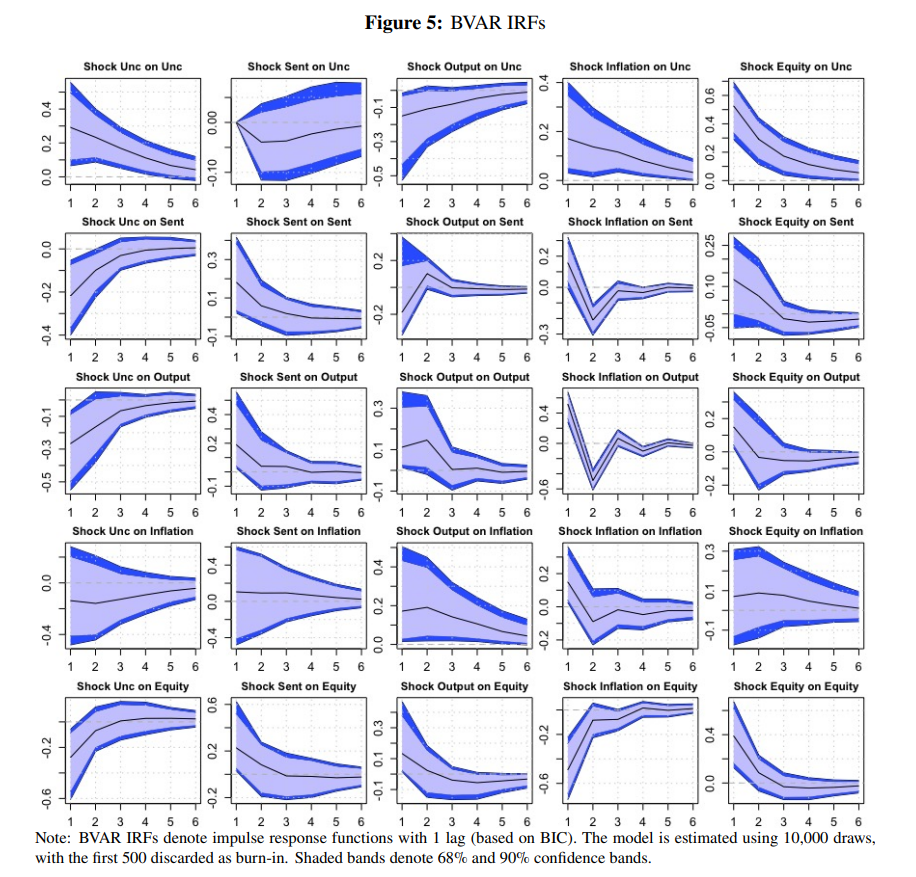

NEW WORKING PAPER: This paper examines the dynamic effects of sentiment on international equity returns using two complementary empirical approaches. First, we estimate panel Local Projections (LPs) for 31 advanced and emerging economies over the period 1996-2023 to trace the response of real equity returns to sentiment shocks. We define a sentiment shock as the innovation in sentiment that is orthogonal to uncertainty, thereby isolating sentiment from the broader informational environment in which it is formed. Positive sentiment innovations increase real equity returns on impact, but the effect is short-lived and dissipates within two quarters. The estimated responses are larger for emerging markets than for advanced economies, although the confidence intervals overlap. Second, we estimate a global Bayesian Vector Autoregression (BVAR) based on common international factors. The BVAR results indicate that sentiment shocks influence short-run global macrofinancial dynamics; however, forecast error variance decompositions and historical decompositions show that sentiment is not a dominant persistent driver of global equity-return fluctuations. Taken together, the panel LP and global BVAR evidence suggest that sentiment innovations primarily act as short-run amplification shocks rather than as persistent sources of international equity-market movements.

You are welcome to download, share, or comment on the following working paper:

- William Ginn, Jamel Saadaoui, and Evangelos Salachas, Sentiment Innovations and International Equity Returns (June 19, 2026). Available at SSRN: 6966198