Financial crises often reveal the political architecture hidden inside monetary plumbing. The Financial Times Alphaville article on swap lines is useful because it does not treat central bank swap lines as merely technical liquidity facilities. It reads them as part of the institutional infrastructure through which monetary power, geopolitical alignment, and access to emergency liquidity are organized.

The key point is that a swap line is not only a contract that can be activated in a crisis. It is also a sign of access. A country may never draw on the line, but the existence of the arrangement tells markets, domestic institutions, and foreign governments that the country belongs to a trusted liquidity perimeter. This is why swap lines are simultaneously macro-financial instruments and instruments of statecraft.

The conventional view: crisis insurance

In the standard macro-financial interpretation, a swap line is crisis insurance. A foreign central bank receives dollars from the Federal Reserve, lends those dollars to domestic institutions facing dollar funding pressure, and thereby limits forced deleveraging, fire sales, and destabilizing exchange-rate pressure. This role was highly visible during the global financial crisis and again during the liquidity stress of March 2020.

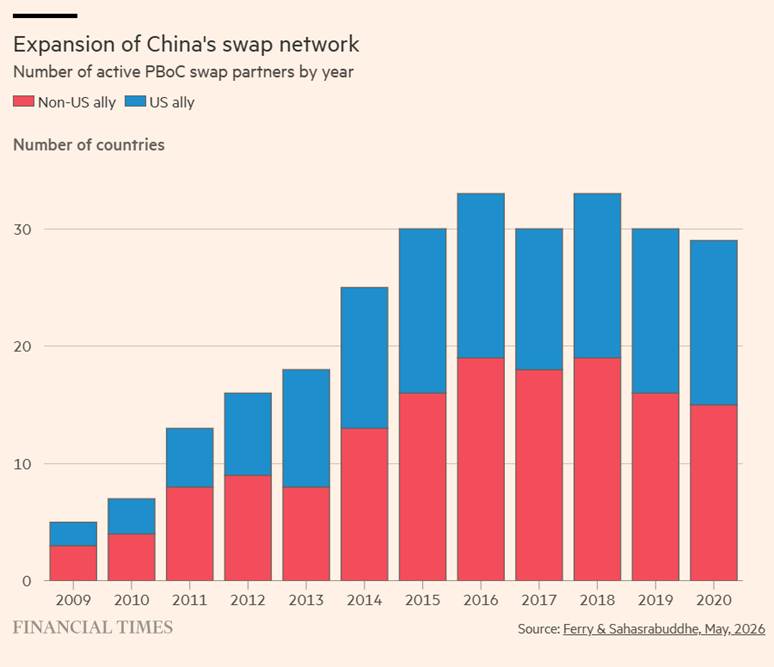

This interpretation explains why the Federal Reserve network is narrow. The standing dollar swap lines are concentrated among close monetary and geopolitical partners: the Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank, and the Swiss National Bank. Temporary extensions may occur in acute stress episodes, but permanent access remains selective. The first FT figure makes this selectivity clear: the Fed network is smaller, while the People’s Bank of China network expanded much more rapidly after the late 2000s.

The geopolitical view: access as alignment

The article’s stronger contribution is to shift the focus from use to access. In this interpretation, swap lines are valuable even when they remain unused. The right to access liquidity in a crisis is itself a form of membership in a monetary-security network. This is why the discussion of potential US dollar swap arrangements with Gulf and Asian partners is politically revealing. When the economic case for emergency liquidity is weak, the geopolitical interpretation becomes stronger.

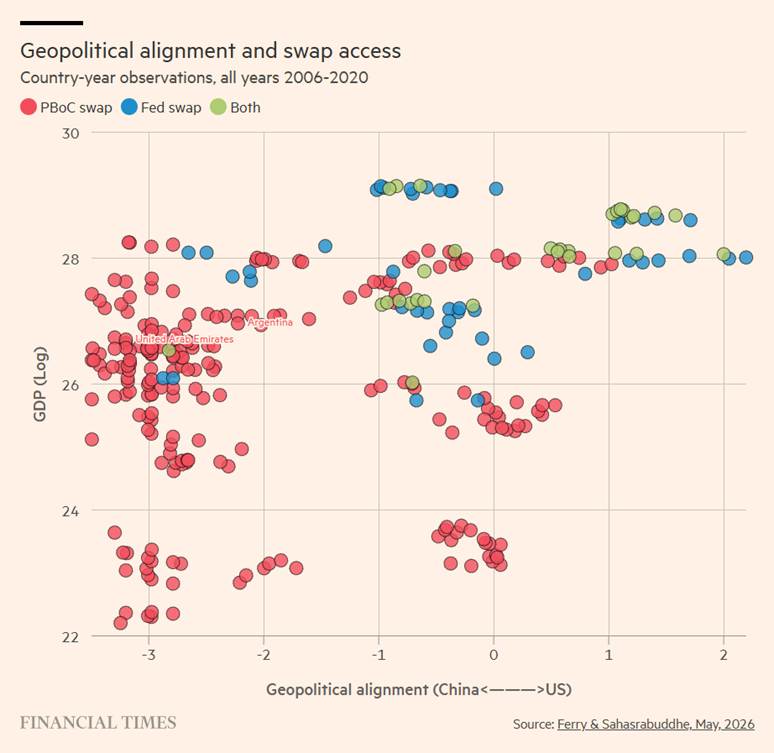

The United Arab Emirates is an especially informative case. A country with large reserve assets and sovereign wealth capacity does not obviously need emergency dollar liquidity in the same sense as a financially fragile economy. A swap-line discussion in that context therefore says less about immediate balance-of-payments stress than about strategic proximity, monetary trust, and the desire to preserve influence over partners that also interact closely with China.

China’s network and the logic of monetary hedging

China’s renminbi swap-line network changes the meaning of dollar access. The PBoC network has been justified by trade settlement, renminbi internationalization, and cross-border liquidity support. Yet the wider the network becomes, the more it also functions as an alternative layer of monetary infrastructure. It does not displace the dollar system, but it gives partner countries another relationship to activate in moments of stress or strategic uncertainty.

The second FT figure shows that the PBoC network expanded quickly after 2009, including among countries that are not US defense allies. This pattern is important because it suggests that swap lines can follow a different logic from traditional security alliances. Some countries can be integrated into China’s monetary network without exiting the dollar system. This is the political economy of hedging: countries diversify monetary relationships while preserving access to the dominant dollar infrastructure.

Alignment, size, and access

The alignment figure is particularly useful because it clarifies that access to swap networks is not explained by economic size alone. Larger economies are more likely to matter systemically, but geopolitical alignment shapes which liquidity network they enter. Countries close to the United States are more likely to appear in the Fed perimeter, while countries closer to China or outside the core US alliance structure are more likely to enter the PBoC perimeter.

This does not mean that central banks mechanically allocate swap lines according to alliance scores. The empirical picture is more subtle. Economic size, financial linkages, trade exposure, reserve needs, institutional credibility, and foreign-policy alignment all interact. The important lesson is that swap lines are not neutral pipes. They are located in a broader structure of international political economy.

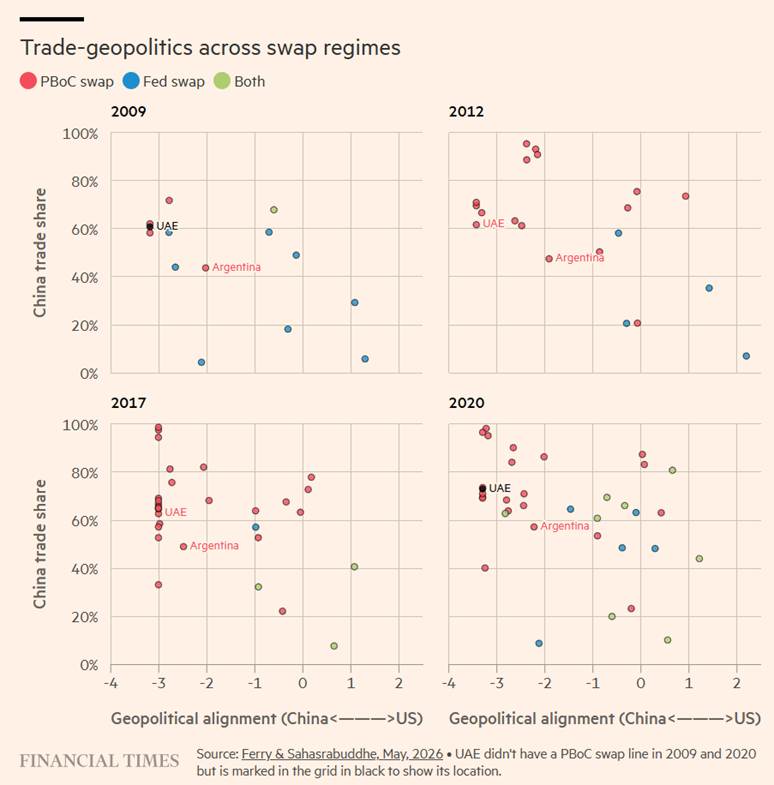

Trade-geopolitics across swap regimes

The trade-geopolitics panels add a further dimension. They show that countries with high China trade shares can occupy different positions in the geopolitical alignment space and in the swap-line architecture. This is a central feature of contemporary globalization: commercial exposure to China does not necessarily imply full geopolitical alignment with China, and security proximity to the United States does not necessarily prevent deep trade links with China.

This matters for macroeconomics because liquidity networks can become binding precisely when trade and finance are politically strained. A country that trades intensively with China, holds dollar liabilities, and maintains security links with the United States may value both sets of relationships. Swap lines then become part of a broader portfolio of geopolitical insurance.

The Exchange Stabilization Fund issue

One institutional complication concerns the difference between a Treasury-led arrangement through the Exchange Stabilization Fund and a Federal Reserve standing swap line. These instruments may both provide dollar liquidity, but they do not carry the same institutional meaning. The Fed’s standing swap lines are embedded in central banking routines, crisis-management norms, and long-standing relationships among monetary authorities. A Treasury-led arrangement is closer to an explicitly strategic instrument of US financial diplomacy.

This distinction is essential for interpretation. If a country receives access through a channel that is less central-bank-based and more foreign-policy-based, the arrangement may be best understood as a hybrid instrument: part financial backstop, part diplomatic signal, part strategic reassurance.

Implications for the euro area

The euro area occupies a privileged position in this architecture. It is part of the Fed’s standing dollar swap-line network through the European Central Bank, and it also has a liquidity relationship with China through the ECB-PBoC arrangement. This position reflects both the euro area’s systemic importance and its ambiguous role in a world of monetary fragmentation: it is a core pillar of the dollar-centered system, but it also interacts with China’s expanding monetary infrastructure.

The European lesson is not that swap lines substitute for deeper capital markets or a stronger international role for the euro. They do not. The lesson is that international currencies are supported by institutions as much as by market size. The dollar’s centrality rests not only on Treasury market depth, but also on the network of credible backstops around it. A more international euro would require not only safe assets and market depth, but also a stronger institutional capacity to provide liquidity internationally.

What economists should take from the debate

Economists should not separate the economic and geopolitical interpretations too sharply. Swap lines stabilize markets because they are credible. They are credible because they are backed by institutions. Those institutions are embedded in political relationships. The same instrument can therefore operate through several channels at once: liquidity insurance, confidence effects, alliance signaling, and monetary-network formation.

This is why the article is relevant beyond the narrow debate on central bank facilities. It shows how the international monetary system is increasingly shaped by infrastructure competition. Payment systems, reserve assets, swap lines, repo facilities, sanctions capacity, and trade invoicing are all part of the same broader contest over monetary power.

Conclusion: monetary plumbing is statecraft

The main lesson is that global monetary power is built through networks. Some networks are visible, such as trade agreements and military alliances. Others are more discreet, such as central bank swap lines, repo facilities, reserve arrangements, and payment infrastructures. But in moments of stress, these discreet networks become decisive.

Swap lines are therefore not only technical instruments. They are geopolitical infrastructure. They define who can access liquidity, whose balance sheet anchors confidence, and which countries are inside or outside the trusted perimeter of the international monetary system. In a world of fragmented globalization, that perimeter is becoming more politically meaningful.

Sources

- Aditi Sahasrabuddhe, “Swap lines are geopolitical infrastructure,” Financial Times Alphaville, May 2026: link.

- Federal Reserve Bank of New York, “Central Bank Swap Arrangements,” for the institutional description of standing dollar liquidity arrangements.

- Board of Governors of the Federal Reserve System, “Central Bank Liquidity Swaps,” for the operation and purpose of dollar and foreign-currency liquidity swaps.

- European Central Bank, “Central bank liquidity lines,” for the general definition of swap and repo liquidity lines in international funding markets.