Today, let me draw your attention to two recent papers published in the Journal of Econometrics that deal with the Local Projection (LP) method introduced by Òscar Jordà in the literature in 2005. This method is often used in empirical research in macroeconomics. The widespread use of this method for computing impulse response functions (IRF) can be explained by its simplicity. Recently, Stata introduced a built-in package to estimate IRF with the LP method in a time series set up.

These two recent articles aim at exploring the theoretical properties of the LP, especially in terms of bias.

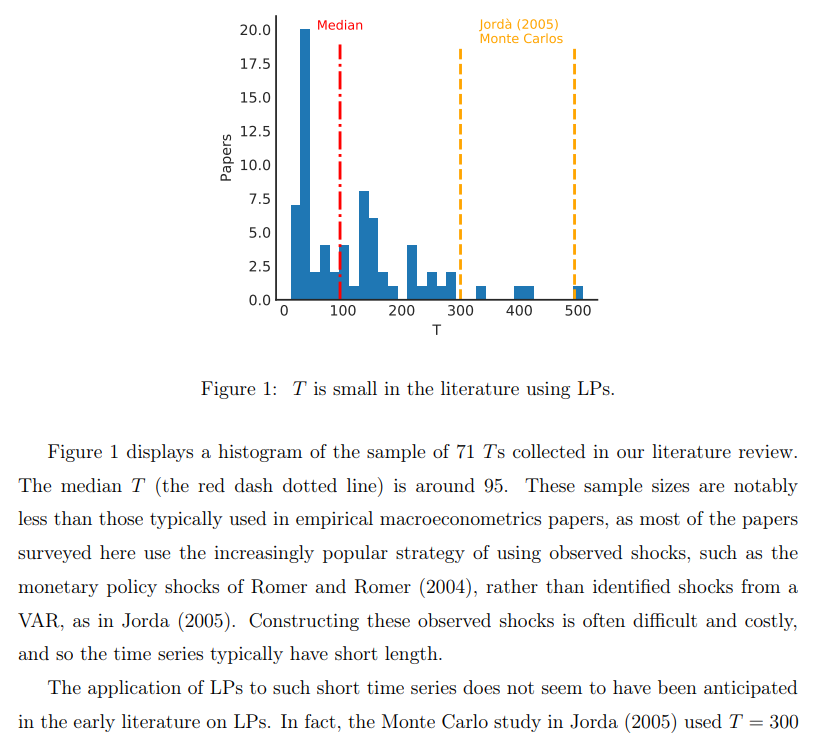

In the first paper, the authors show that using a time series setting with T up to 200 may produce a substantial bias in the IRF (inference is not examined in their paper). They also show that using a panel setting with N up to 50 may also produce a substantial bias.

Herbst, E. P., & Johannsen, B. K. (2024). Bias in local projections. Journal of Econometrics, 240(1), 105655. S0304407624000010.

Ungated version (prepublication): bias-in-local-projections.

In the second paper, the authors discuss the bias in state-dependent LP and, especially, when the state-dependent variable is not exogenous. They show that state-depend LP are valid when the state-dependent variable is exogenous or endogenous when “the shock of interest is smaller than the sample standard deviation of the exogenous policy shock series”. This latter case being not realistic in many applications in macroeconomics.

Gonçalves, S., Herrera, A. M., Kilian, L., & Pesavento, E. (2024). State-dependent local projections. Journal of Econometrics, 105702. S0304407624000484.

Ungated version (prepublication): https://silvia-goncalves.research.mcgill.ca/

Please find below a very pedagogical presentation by Silvia Goncalves on a previous version of the paper. When the state variable is endogenous, they show that the bias is asymptotic, and consequently, cannot be reduced by an increasing T.

As applied researchers, we can learn from these two recent articles that, if you would rather not use a bias-corrected method, LP should be used with a long-time dimension (at least T>200) and a large cross-section of individuals (at least N>50). Furthermore, state-dependent LP should be used with an exogenous transition variable.

1 Comment

[…] Two recent articles on Local Projections […]